Quantile Regression for Weather Risk Pricing

A weather prediction market does not need a forecast. It needs odds. I built the ML layer for one as a CS 506 team project: models that quote risk-adjusted prices on temperature, wind speed, and precipitation outcomes.

Ensembles require uncorrelated errors

I started with an averaging ensemble of XGBoost, RandomForest, and LightGBM. It achieved 5.00°F MAE, identical to XGBoost alone. All three are gradient boosting variants trained on the same features. They fail on the same inputs, so averaging adds nothing.

Stacking with a Ridge meta-model confirmed this: weights of 0.55 (XGBoost), 0.42 (LightGBM), 0.03 (RandomForest). Introducing algorithmic diversity (Ridge, SVR, MLP alongside XGBoost) didn't help either; the meta-model assigned 80% weight to XGBoost. A single tuned model outperformed every ensemble configuration.

I took the result to my research advisor, whose background is in meteorology. His read was that 5°F is roughly the error floor for a single-source model on this kind of target. I had not undertuned anything; I had run out of data. The point forecast was not going to improve without ingesting sources I did not have. But the platform did not need a better point forecast. It needed to know how confident the forecast was.

Point predictions to distributions

5.00°F MAE is a reasonable point forecast, but point predictions can't set odds. 77°F doesn't tell the platform whether that's a confident prediction or a volatile one. Pricing wagers requires the model to output a distribution, not a number.

XGBoost supports quantile regression natively via reg:quantileerror. I trained three models (P10, P50, P90) per target:

base_model = xgb.XGBRegressor(

objective='reg:quantileerror',

quantile_alpha=quantile, # 0.1, 0.5, or 0.9

random_state=RANDOM_SEED,

n_jobs=-1,

tree_method='hist'

)

The P10/P90 outputs define an 80% prediction interval. The spread (P90 - P10) is the risk signal: 4°F means tight odds, 9°F means the house widens its margin.

Feature engineering produced 90 candidates -- cyclical temporal encodings, rolling windows (3/7/14/30-day), lag features, meteorological interactions. RFECV reduced that to 11-16 per target. Hyperparameter tuning used Optuna with TimeSeriesSplit to avoid temporal leakage. The pipeline serializes twelve artifacts: one feature selector and three quantile models per target.

Final MAE: 4.35°F on a held-out test set, down from 5.00°F.

Calibration

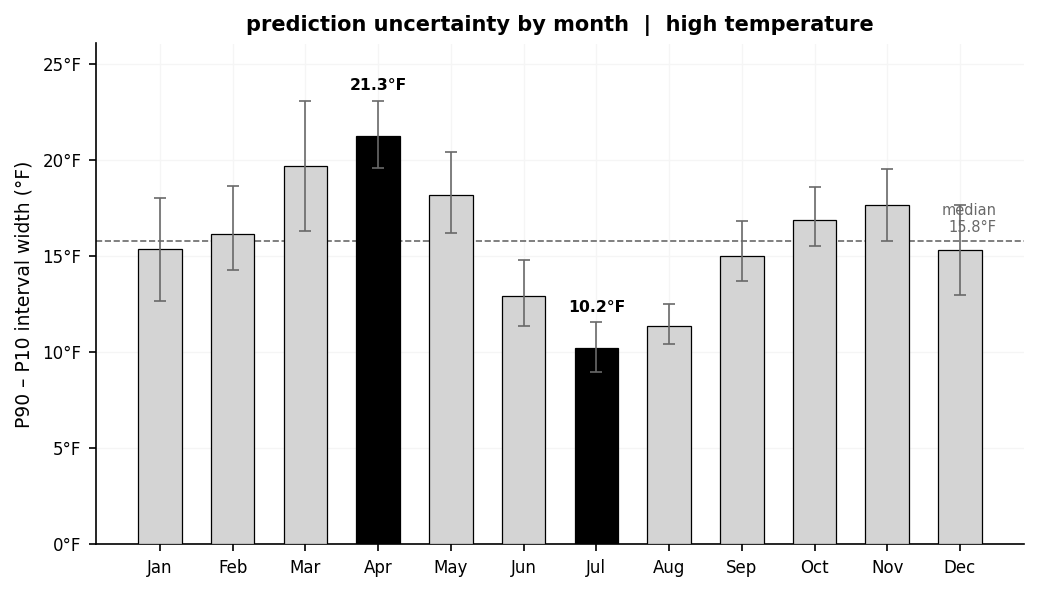

On the held-out set, P10-P90 intervals captured actuals 81-85% of the time across all three targets (nominal: 80%). Backtesting confirmed the house margin converges to the 10% target.

The intervals also track seasonal volatility: April averages 21°F wide, July averages 10°F. The model had learned that spring is harder to predict than midsummer and was widening its quotes accordingly. A single fixed margin would have either over-quoted in summer or under-quoted in spring.

I later ported this pipeline to CardinalCast, a standalone Python/FastAPI implementation.